Raju Rastogi is an employee with an MNC with a handsome salary. He visited and celebrated the new year with his close friend Farhan Qureshi in Dubai. When he was in Dubai, he had identified a flat in Dubai and after much discussions, decided to purchase it as an investment. Since the flat booking timeline available was short, Raju planned to request Farhan to make the 20% of booking advance on his behalf to freeze the deal. He thought that he can reimburse him in his mother’s bank account in India as this is easier. Is Raju on the right track?

Bona Fide Transaction?

Asking a friend residing abroad to pay for the booking advance of a flat on your behalf could sound like a harmless, straight forward transaction. Most of the time, such decisions are taken hurriedly, without consulting an expert. But this simple, seemingly harmless transaction can be construed as violation of the Foreign Exchange Management Act (FEMA) !

What does the Enforcement Directorate say?

As per recent news, the Enforcement Directorate (ED) is understood to have questioned individuals who had let a friend or a partner residing abroad to pay on their behalf the initial deposit or reserve money of 10 to 20%. The actual buyer, Resident Indian, pays the balance amount directly to the foreign seller and separately pays off the friend either in cash or bank transfer, or some other adjustments. News says that the ED has invoked Section 3(a) of FEMA, which is typically used against hawala operators in notice served to such persons.

FEMA regulates forex transactions

FEMA regulates transactions between residents and non-residents (NRIs/PIOs) to control foreign exchange, requiring all transactions to occur through authorized banking channels. FEMA requires that all foreign currency transactions between a resident and a non-resident be routed strictly through normal banking channels, with no exemptions – irrespective of the amount or purpose of payment.

What are the options available?

For time-sensitive obligations, individuals may rely on funds already remitted and retained abroad under the Liberalised Remittance Scheme (LRS), provided the underlying use remains within permitted transactions. Under LRS, a resident individual can buy properties and stocks as well as carry out current account expenses on travel, medical care, and gifts up to $250,000 a year.

Disclosure of Foreign Assets in ITR and consequences of mismatch:

Such assets acquired in foreign lands have to be disclosed (along with their investment value) under schedule FA in the Income tax returns. A mismatch in the value of an asset and the balance amount of 80% transferred by the buyers through banks can trigger red flags and the tax officials may share information with the ED as a normal protocol. LRS details like the amounts and the identities of the local payer and the non-resident recipient are routinely shared with the Reserve Bank of India.

Consequence of seemingly harmless transaction:

Significantly, the offences under section 3(a) are compoundable only by ED, and RBI. Even if persons who have received a notice are in a position to close the matter eventually, they would have to go through the pain of hiring a lawyer, dealing with the questions from the ED, sharing copies of passports and bank account details for earlier years, etc.

NRI and related tax issues

In spite of shifting base to different geographies, many Indians keep in touch with their roots, tradition, culture and rituals as that has been the way our DNAs are made!

Income tax as a subject by itself undergoes numerous changes every year and it could be quite cumbersome to keep a tab on the innumerable changes. Recent changes to the Income Tax Act changed the way NRIs are taxed in India. With the introduction of the term “deemed resident”, it becomes all the more important to review the residential status every year. The Income Tax law is more stringent now and has more tools to track and tap information to enable effective taxing of the NRIs.

Being an NRI, you have to deal not with one but with at least two country’s tax laws. We understand your needs and can be of tremendous support in keeping tax compliance in India on track. Our NRI services can help you save time and effort, while also minimizing the risk of penalties and legal issues arising from non-compliance with tax laws.

-

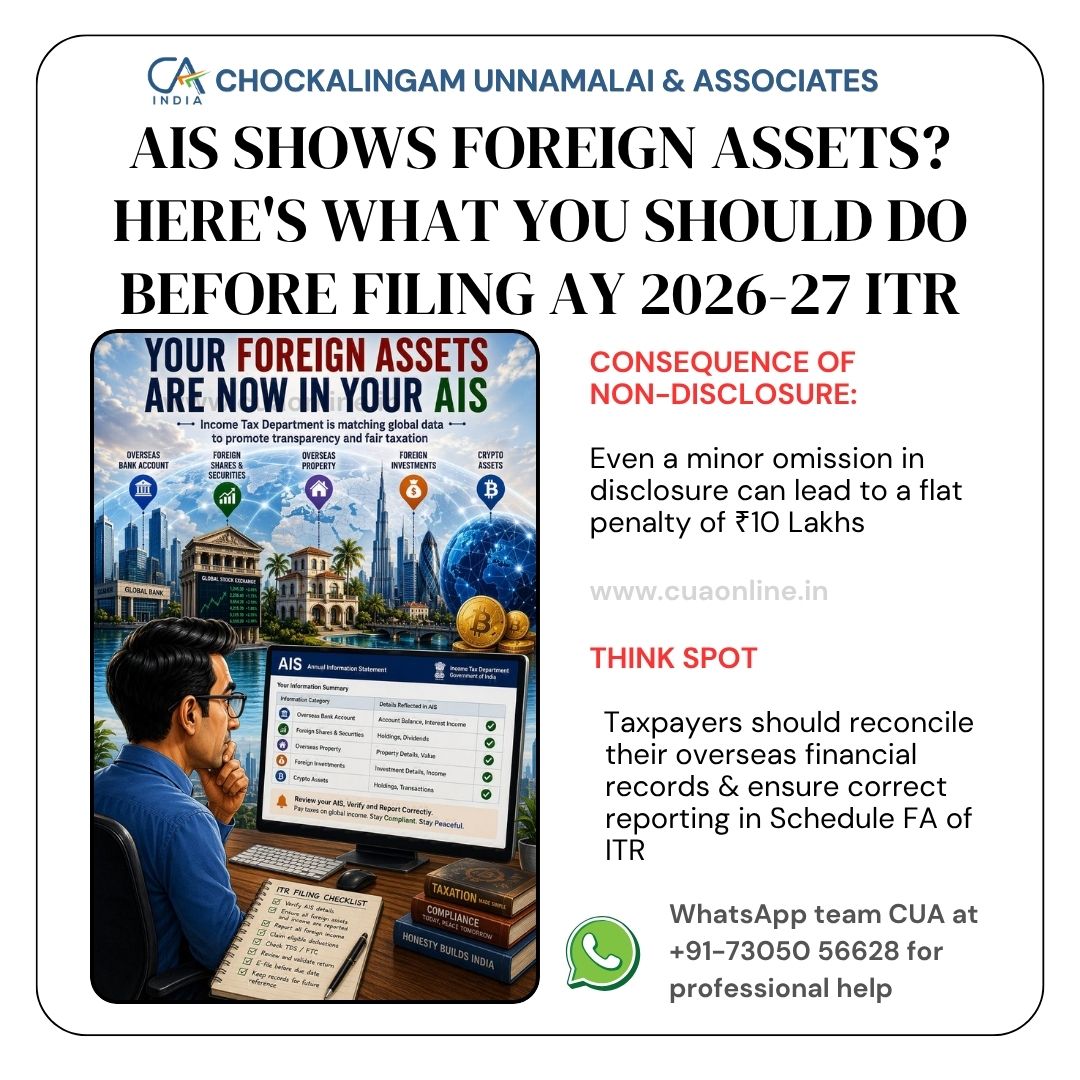

AIS Shows Foreign Assets? Here’s What You Should Do Before Filing AY 2026-27 ITR

Vetri Kondan was allotted ESOP shares when he was working for an MNC having its offsite DC in Chennai. He quit his job and pursued his freelance career as a consultant. Vetri’s AIS reflects Foreign Assets and dividend income from calander year 2022 to 2024. He had not disclosed his foreign assets nor the income…

-

Can paying off your home loan help you save capital gain tax?

Raju Rastogi is a an employee with an MNC with a handsome salary. He visited and celebrated the new year with his close friend Farhan Qureshi in Dubai. When he was in Dubai, he had identified a flat in Dubai and after much discussions, decided to purchase it as an investment. Since the flat booking…

-

Paying booking advance through a friend in Dubai for a flat purchase risks FEMA violation!

Raju Rastogi is a an employee with an MNC with a handsome salary. He visited and celebrated the new year with his close friend Farhan Qureshi in Dubai. When he was in Dubai, he had identified a flat in Dubai and after much discussions, decided to purchase it as an investment. Since the flat booking…